Shifting Multifamily Supply / Demand Dynamics

Written by Chicagoland 1031 Exchange on October 10, 2025

Over the last several years, multifamily housing has experienced an unprecedented surge in new development. Fueled by strong demand, high occupancy, and historically low interest rates, developers pushed construction activity to levels not seen since the 1970s.1

Now that story is changing, and for property owners and investors, this shift points to a more favorable environment.

New Construction Starts Are Falling Nationwide

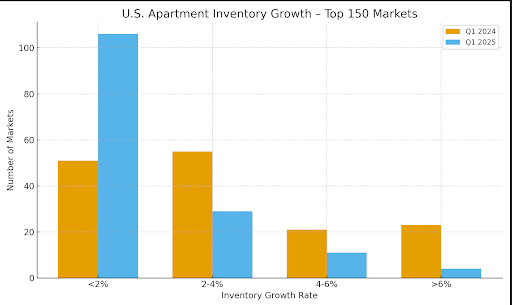

Across the top 150 U.S. markets, apartment inventory growth is retreating from historic highs. In 2023 and 2024, nearly one-third of markets grew supply by more than 4%. By 2025, that number is expected to drop considerably, with more than 100 markets seeing inventory expand by less than 2%—the lowest level since the aftermath of the Global Financial Crisis.

This slowdown isn’t confined to one region. Sun Belt markets like Austin and Nashville saw outsized development in recent years and are now seeing supply expansion cut by nearly half. Gateway markets such as Boston are experiencing muted growth as well, with inventory projected to rise by just 2.6% in 2025.1

Demand Remains Resilient

Demand for rental housing remains historically strong, and there are a number of factors1 pointing towards this trend continuing:

- The median first-time homebuyer is now 38, meaning households are renting longer

- Vacancy rates remain below long-term averages

- Absorption (net new renter households) has exceeded expectations in both 2024 and early 2025

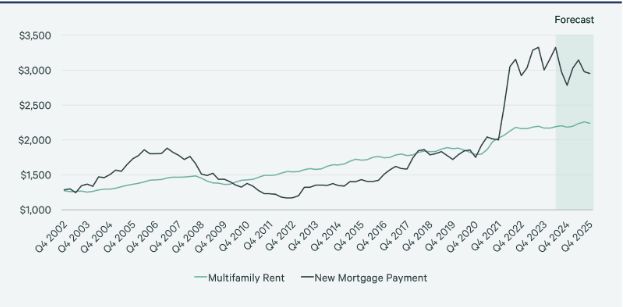

- Mortgage rates have dropped from their peaks; however, the affordability gap between renting and home ownership remains historically large

Meanwhile, new deliveries are expected to fall dramatically. Between 2020-2024, the market delivered an average of 515,000 units per year. Forecasts over the next five years show new completions dropping to just 317,000 units annually.1

Future Outlook

This “supply cliff” sets the stage for a period where demand is likely to outpace supply, creating upward pressure on rents. Importantly, once this trend sets in, it will be difficult to slow down as multifamily development typically involves long timelines. On average, projects take around 29 months from permitting to completion.2

What This Means for Investors

For multifamily property owners, slowing supply and steady demand gains are creating an environment where rent growth is likely poised to accelerate. With fewer new units competing for tenants, owners may regain pricing power, improving both operating income and asset values.

For investors considering 1031 exchanges or new acquisitions, the current market represents a potentially appealing entry point. As new supply continues to taper, the ability to capture rental growth could translate into attractive long-term returns.

At Chicagoland 1031 Exchange, we believe these dynamics reinforce multifamily housing as a compelling hedge against inflation and a resilient income-producing asset class to diversify investors’ portfolios. We also continue to see multifamily investing as a cornerstone of 1031 exchangers’ replacement property allocations.

If you have any questions or want to learn more, we’re here to help. Talk to one of our advisors today.

1. CoStar, as cited in the Griffin Capital Market Research Note – Multifamily Supply Trends (July 31, 2025).

2. Griffin Capital

Are you ready to talk?

Whether you're thinking about selling a property and want to better understand the 1031 exchange process and investment choices, or if you already sold your property and the proceeds are currently held at a Qualified Intermediary, we can help.

Please call us at (224) 245-5281 or schedule an introduction today.

Chicagoland 1031 Exchange proudly serves clients nationwide, including California, Illinois, Florida, Colorado, Massachusetts, and more.

The information herein has been prepared for educational purposes only and does not constitute an offer to purchase or sell securitized real estate investments. Such offers are only made through the sponsors Private Placement Memorandum (PPM) which is solely available to accredited investors and accredited entities. DST 1031 properties are only available to accredited investors (typically have a $1 million net worth excluding primary residence or $200,000 income individually/$300,000 jointly of the last two years, and reasonably expects the same for the current year) and accredited entities only. If you are unsure if you are an accredited investor and/or an accredited entity please verify with your CPA and Attorney. There are risks associated with investing in real estate and Delaware Statutory Trust (DST) properties including, but not limited to, loss of entire investment principal, declining market values, tenant vacancies and illiquidity. Potential cash flows/returns/appreciation are not guaranteed and could be lower than anticipated. Because investor’s situations and objectives vary this information is not intended to indicate suitability for any particular investor. This material is not to be interpreted as tax or legal advice. Please speak with your own tax and legal advisors for advice/guidance regarding your particular situation.

This site is published for residents of the United States only. Representatives may only conduct business with residents of the states and jurisdictions in which they are properly registered. Therefore, a response to a request for information may be delayed until appropriate registration is obtained or exemption from registration is determined. Not all services referenced on this site are available in every state and through every advisor listed. For additional information, please contact Nathan Kuhn at 224-245-5281.

Chicagoland 1031 Exchange does not offer legal or tax advice. Please consult the appropriate professional regarding your individual circumstances.

Securities offered through DAI Securities, LLC, member FINRA / SIPC. Advisory services offered through Kuhn Wealth Management, Inc. (KWM), a state registered investment advisor. Insurance offered through DAI Securities, LLC. KWM dba Chicagoland 1031 Exchange is independent of DAI Securities, LLC.